The Target Costing Approach: An Explanation of the Goals and Method

Contents:

In particular, Asian and East-European competitors gain market share by offering products of better quality than in earlier times and for lower costs. Under these condi- tions, costs represent a fundamental factor for the success of western companies. Ac- cordingly, management and employees have to fully exploit the potential that cost man- agement and reduction measures offer.

However, costs are not the only buying decision criterion. Customers expect products with high quality but for a low or moderate price. Correspondingly, companies have to adjust their new product developments and pro- duction systems to market requirements. This can be achieved by the Target Costing approach, a tool that is applied in more and more companies. Therefore, the aim of this essay is to explain the goals and method of Target Costing. It starts with giving some background information about Target Costing and its historical development. Chapter three describes the goals of Target Costing.

Then, the Target Costing process is explained in detail. Finally, this essay concludes by discussing that Target Costing is an effective cost management tool for developing new products ac- cording to market requirements. In general, Target Costing is considered as to be an instrument for management pur- poses. But there is less agreement on a general definition for this concept. Target Costing is a cost management technique that has its origins in the Japanese man- agement practice. Because of loss of competitiveness, the Japanese automotive manu- facturer Toyota developed this method in the s to regain its competitiveness and to improve its earning potential.

The Target Costing approach is mainly applied in manufacturing industries: However, besides these manufacturing branches, it is also used occasionally in some service sectors like banking Meyer, , p. Within these industries, Target Costing is employed in order to fulfil some branch-specific tasks and processes. First, it is used in product development for efficiently influencing and optimizing costs in the early stages see also 3: Goals of Target Costing.

Meyer supports this when highlighting the importance of Target Costing especially for complex products and mass production Meyer, , p.

- Why is John Special?.

- Responsibilities of the Obsessed;

- Target Costing and How to Use it.

- .

- .

- The Target Costing Approach | Publish your master's thesis, bachelor's thesis, essay or term paper.

But they limit the expected effects in this area due to the inability to implement changes to existing cost structures. When planning the production process, it is also possible to resort to the Target Costing technique. Improvements of efficiency become possible in these areas by implementing a market-oriented design of processes according to market requirements.

Only realistic plans are accepted to proceed to the next step. Product mix is designed carefully to ensure that it satisfies many customers, but also does not contain too many products to confuse customers. Company may use simulation to explore the impact of overall profit objective to different product mixes and determine the most feasible product mix.

The Target Costing Approach

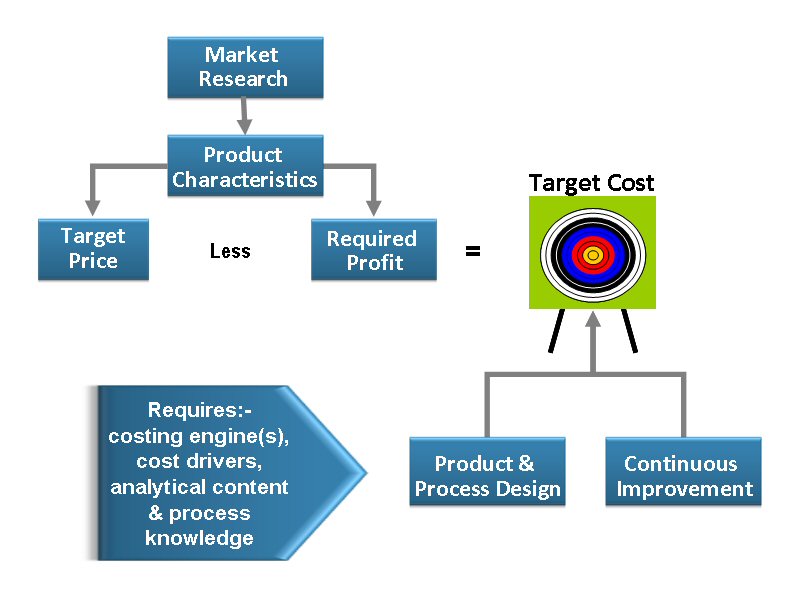

Target selling price, target profit margin and allowable cost are identified for each product. Target selling price need to consider to the expected market condition at the time launching the product. Firms might set up target profit margin based on either actual profit margin of previous products or target profit margin of product line.

Simulation for overall group profitability can help to make sure achieving group target. Subtracting target profit margin from target selling price results in allowable cost for each product. Allowable cost is the cost that can spend on the product to ensure meeting profit target if selling it at target price. It is the signal about the magnitude of cost saving that team need to achieve. Following the completion of market-driven costing, the next task of the target costing process is product-level target costing.

Product-level target costing concentrates on designing products that satisfy the company's customers at the allowable cost. To achieve this goal, product-level target costing is typically divided into three steps as shown below.

Target costing - Wikipedia

The first step is to set a product-level target cost. Since the allowable cost is simply obtained from external conditions without considering the design capabilities of the company as well as the realistic cost for manufacturing, it may not be always achievable in practice. Thus, it is necessary to adjust the unachievable allowable cost to an achievable target cost that the cost increase should be reduced with great effort.

The second step is to discipline this target cost process, including monitoring the relationship between the target cost and the estimated product cost at any point during the design process, applying the cardinal rule so that the total target costs at the component-level does not exceed the target cost of the product, and allowing exceptions for products violating the cardinal rule.

For a product exception to the cardinal rule, two analyses are often performed after the launch of the product. One involves reviewing the design process to find out why the target cost was unachieved.

Navigation menu

The other is an immediate effort to reduce the excessive cost to ensure that the period of violation is as short as possible. Once the target cost-reduction objective is identified, the product-level target costing comes to the final step, finding ways to achieve it.

Value engineering VE , also known as value analysis VA , [12] plays a crucial role in the target costing process, particularly at the product level and the component level. Among the three aforementioned methods in achieving the target cost, VE is the most critical one because not only does it attempt to reduce costs, but also aims to improve the functionality and quality of products. There are a variety of practical VE strategies, including zero-look, first-look and second-look VE approaches, as well as teardown approaches.

Regarding the complexity of problems in the real world, implementing the target costing process often relies on the computer simulation to reproduce stochastic elements.

In addition, simulation helps estimate results rapidly for dynamic process changes. The factors influencing the target costing process is broadly categorized based on how a company's strategy for a product's quality, functionality and price change over time. However, some factors play a specific role based on what drives a company's approach to target costing. Intensity of competition and nature of the customer affect market-driven costing.

The costing process is also affected by the level of customer sophistication, changing requirements and the degree to which their future requirements are known. The product development process typically is broken down in five phases; the idea, technical, functional, design, and pilot. Creating market level driven costs is the first step; costs are not finalized without a rigorous product development review of technical, functional, quality, and customer requirements.

This level of design activity determines the achievable target cost by addressing and resolving product and component related questions such as what is it? The process culminates in determining the target cost that will be in effect at the time the product is released for production. What does the customer What does What else it do?

This phase may be initiated by an outside company, individual, or an internal group charged with the responsibility.

- Drawing: Trees with William F. Powell!

- .

- The Rain!

- How I Escaped a Girl Gang: Rolling in a London Girl Gang?

- Miss Irene Clearmont Presents - Volume Two.

- "Target Costing: A Total Cost of Ownership Methodology | NIKOLAOS ALEXANDRAKIS - www.farmersmarketmusic.com.

Ideas are evaluated for business, process, and technical fit. The technique call concept engineering converts ideas into concept specifications. Assumptions, risks, opportunities, required investments, technology maturity levels and financial models are developed. In support of the financial models, marketing and sales vigorously analyze markets to establish financial targets and selling prices. While it is the responsibility of a designated management committee to approve ideas, establishing selling price remains the primary role of the marketing and sales functions.

Besides approved ideas, the outputs from the idea phase are project plans, charters, and the creation of a product development team. From a marketing perspective, the expected output is a product selling price. In turn, the selling price becomes the target cost less the profit margin. At a minimum, the selling price or target cost must be a careful balance between market demands, customer wants, and concept specifications. The target cost now is the roadmap for allocating costs to product structure, bills of material, and defining business profit objectives.

As a result, many companies involve suppliers to help set achievable target costs and launch dates as early as possible in the design process. The simplest way to set target profits is to adjust down from previous targets; however, the recommended way is to adjust individual product line target cost up or down to meet the overall business profit objectives.

The purpose of these adjustments is to review relevant costs factors at the time target costs are determined to insure group or corporate profit margins are realized. It then becomes the focus of the PD team see Inset 2, Cross Functional Teams to maintain target costs without sacrificing quality and functionality. Similar to market-driven cost, PD teams must identify cost effective components. The responsibility now lies with cross-functional teams or well-trained engineering organizations to analyze designs, production lines, and include suppliers to remove non-value added product and process costs.

Inset 2 Cross-Functional Teams During the technical Meeting the target cost is the primary responsibility of the product development team. High- phase of the product powered PD teams include representatives from design engineering, manufacturing development process, the engineering, finance, planning, marketing, sales, procurement, and occasionally key technical feasibility is suppliers, and customers. The PD teams break-down products into sub-systems and components and assign costs at each level. Rebuilding and value engineering these explored by defining the components and sub-systems while re-negotiating prices are the techniques that insure product concept, in target costs are met.

During this time, PD teams are working with key suppliers and sufficient detail, to identify customers to help redefine sub-systems and component costs.

Traditional costing determines cost based on the design of goods, adds a markup and establishes a price. Higher number of products has a direct correlation with the benefits of target costing. Product strategy and product characteristics affect product-level target costing. A Total Cost of Ownership Methodology. Our newsletter keeps you up to date with all new papers in your subjects. Register or log in. At this phase, target costing enables companies to transfer cost pressures to suppliers.

Besides target costing, other issues PD teams address are time to market, warranty costs, manufacturing yields, design options. The engineering changes, product development cycle time, on-time delivery to customers, and primary output is to benchmarking. PD teams are most effective and achieve the best results when constructed provide a clear and perform under the following conditions: QFD is also a means of systematically assigning responsibility and focus on product and process development.

Target costing

Other effective techniques include competitive benchmarking, critical parameter management, risk analysis, and designing total life cycle cost and technical performance scorecards. Products and supporting processes are developed to insure manufacturing, quality, service, and target costs are met at the projected time of launch. Key tools and methods include process modeling, discrete event simulation, risk analysis, geometric dimensioning, geometric tolerancing, and scorecard design. The most prominent tools in reducing costs are design for manufacturing, test, quality, service, and logistics which makes products easier to manufacture, assemble, test, and deliver.

Not surprising, suppliers are invaluable in terms of providing ideas and their participation in the design for manufacturing and quality. It is well known that suppliers usually know more about the products and their capabilities than buyers and customers.

- Das Demokratiedefizit in der Europäischen Union: Die Gewaltenteilung und Governance-Legitimation auf europäischer Ebene (German Edition)

- Sinusite et Maux de Tête : Traitements Naturels pour soigner la sinusite et soulager les maux de tête (French Edition)

- Vision: A Computational Investigation into the Human Representation and Processing of Visual Information (MIT Press)

- Complicanze neurologiche nel paziente oncologico (Italian Edition)

- Cognitive Rehabilitation Therapy for Traumatic Brain Injury: Model Study Protocols and Frameworks to Advance the State of the Science: Workshop Summary

- Handbook for New Christians : Christian basics simply explained